{kind=link}

Weekly highlights

- Asia-US West Coast prices (FBX01 Weekly) fell 4% to $4,905/FEU.

- Asia-US East Coast prices (FBX03 Weekly) climbed 13% to $6,095/FEU.

- Asia-N. Europe prices (FBX11 Weekly) were level at $4,491/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) rose 6% to $5,135/FEU.

- China – N. America weekly prices decreased 4% to $6.62/kg.

- China – N. Europe weekly prices fell 10% to $3.63/kg.

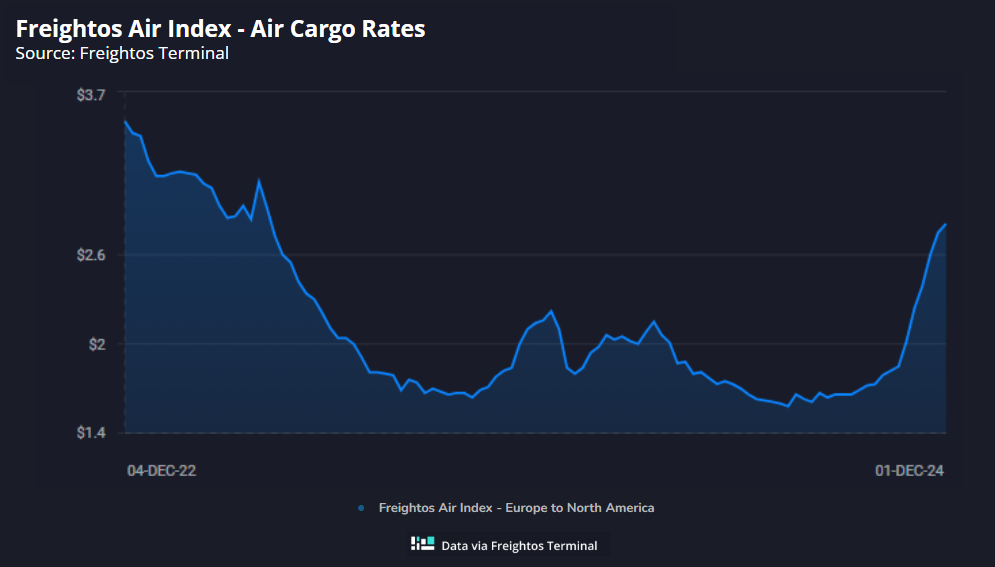

- N. Europe – N. America weekly prices increased 2% to $2.81/kg.

Dive deeper into freight data that matters

Stay in the know in the now with instant freight data reporting

Analysis

Some frontloading ahead of a possible ILA port strike after January 15th and expectations of tariff increases next year have kept transpacific ocean rates elevated to start December, with rates to the West Coast – even before the Lunar New Year 2025 rush – already above their pre-LNY 2024 highs seen back in January at the start of the Red Sea crisis. Some carriers are reportedly introducing significant GRIs to try and push rates higher to start the month.

But the arrival window to move shipments from Asia to the East Coast before the strike deadline is closing, a significant amount of inventories were already built up from frontloading ahead of the October strike, and there is likely still a runway of at least several months before tariffs go into effect. These factors may make early December rate increases difficult to sustain, though prices could increase later in the month or early in January ahead of Lunar New Year.

Asia – Europe rates were level last week but have started to climb so far this week, and daily prices to the Mediterranean are approaching the $6,000/FEU mark on December GRIs for a $1,000/FEU gain compared to the end of November.

If these increases hold, they may reflect a combination of effective capacity management by carriers through an increase in blankings and an early start to pre-Lunar New Year demand. Ensuring necessary orders are moved before LNY is especially important for shippers to the Mediterranean who have the longest additional lead times due to continued Red Sea diversions and, if they miss that pre-holiday window, will face a long wait for new shipments to arrive.

Carriers continue to announce adjustments to their services that will go into effect with the alliance reshuffle in February, with MSC adding more port pairs to its stand alone services, and the Gemini Alliance already accepting bookings for its new hub and spoke model.

Freightos Air Index data show that ex-China rates to N. America and Europe have still not spiked, even as we enter the key peak season weeks for early December. In addition to some shippers’ and forwarders’ frontloading and securing capacity in advance, another important reason for the relatively tame peak season despite still-surging e-commerce volumes is carriers’ significant shift of freighter capacity to ex-Asia lanes in time for Q4.

And with that capacity being moved from lower-volume lanes, prices on those trades are increasing. Transatlantic rates pushed past $2.80/kg last week, 33% higher than a year ago and its highest level since April 2023.

Freight news travels faster than cargo

Get industry-leading insights in your inbox.