{kind=link}

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management. Because when it comes time to rebalance the portfolio to its asset allocation targets – or to reallocate the portfolio to a new strategy – any trades made to implement those changes can generate capital gains, resulting in tax consequences for the investor.

Once a portfolio becomes ‘locked up’, i.e., unable to be managed without triggering capital gains, investors’ options become limited. Charitably inclined investors can donate appreciated securities and avoid gains on the sale. If they don’t plan to use the portfolio funds in their lifetime, they could simply hold the assets for heirs to preserve the stepped-up basis. Otherwise, the investor would traditionally have had to accept that taxes would impose a drag on their portfolio performance going forward.

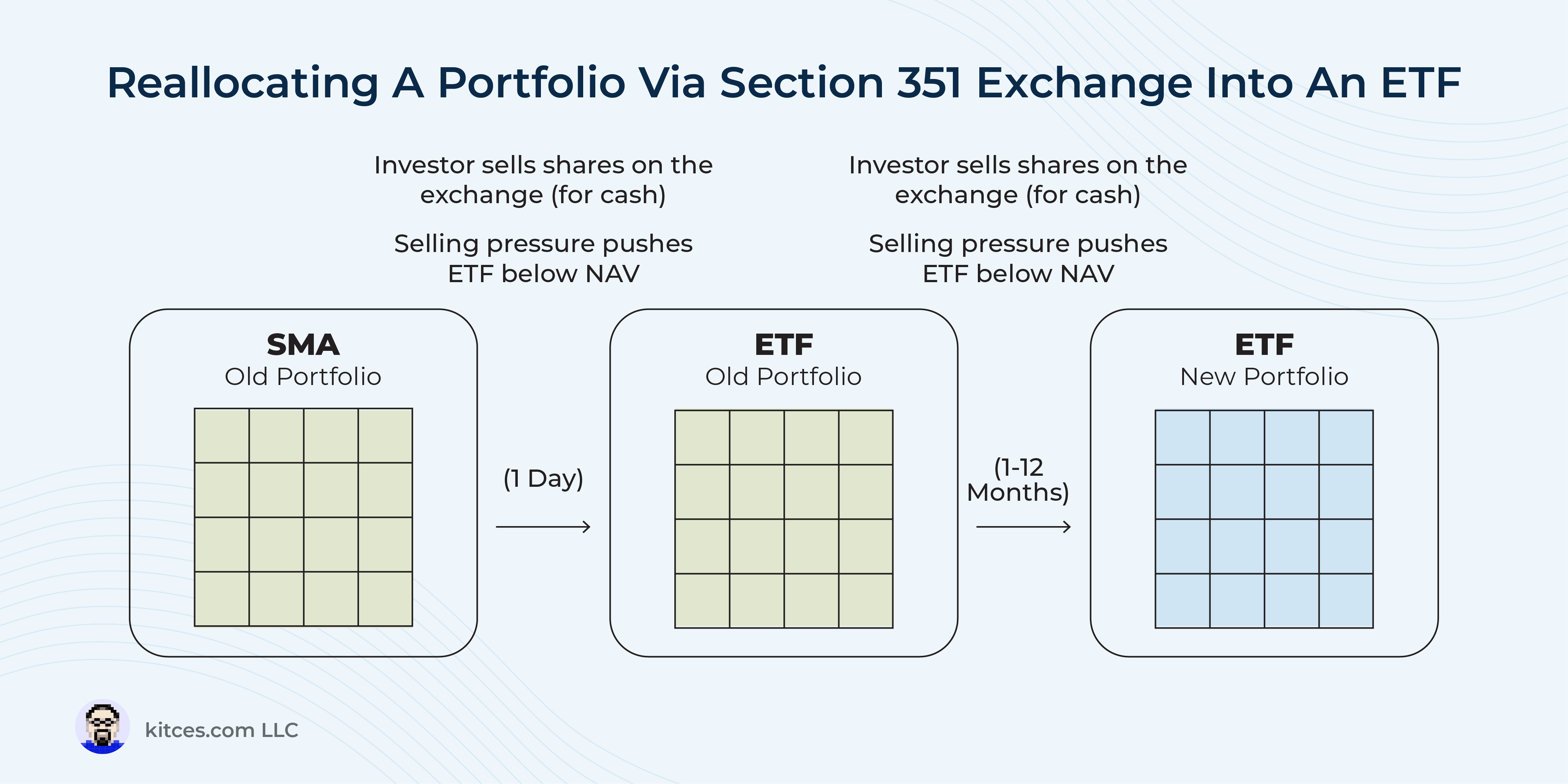

One relatively new strategy, the Section 351 exchange, allows some investors to reallocate assets without triggering capital gains tax. Section 351 allows for tax deferral when assets are transferred to a corporation in exchange for that corporation’s stock, provided the transferor owns at least 80% of the corporation following the exchange. Although the concept of Section 351 exchanges has existed for over a century, it has only recently been applied to individual investment portfolios.

The strategy works by pooling the portfolios of multiple investors in a newly created ETF, with the investors receiving ETF shares in return for the assets that they contributed. If the exchange meets the requirements of Section 351, it is tax-deferred for investors. And once inside the ETF ‘wrapper’, assets can be reallocated with no tax impact for the investors via the tax-efficient ETF structure, which makes use of in-kind creation and redemption of shares. In effect, investors can effectively trade a locked up for an ETF that can be managed with little or no tax impact at all!

However, to meet the requirements for tax-deferred treatment under Section 351, each investor’s portfolio must meet a diversification test, where no single asset can exceed 25% of the portfolio’s value and the top five holdings cannot exceed 50% of the overall value. Additionally, certain assets, like mutual funds, alternative assets, and REITs, may not be eligible for exchange, although other ETFs generally are.

For financial advisors, Section 351 exchanges present a potential solution for clients with high embedded gains, such as those who through the use of tax-loss harvesting have lowered their portfolios’ basis to the point where it’s no longer possible to harvest any losses to offset the gains realized in reallocating the portfolio. Recently, several ETF sponsors have launched ETFs seeded in-kind by individual investors, creating a new channel for advisors who want to take advantage of Section 351 exchanges for clients. Some providers even offer services to help advisors launch their own ETFs seeded by their clients’ funds.

While the options for Section 351 exchanges remain limited – and some advisors may not yet be comfortable recommending them due to their short track record – the strategy is still worth watching. If it gains traction, it could be a helpful tool for advisors to implement more tax-efficient investment strategies – while overcoming the inconvenient tax friction of implementing the strategy to begin with!